You have 3 FICO scores, one for each of the 3 credit bureaus Experian, TransUnion and Equifax. Each rating is based on information the credit bureau keeps file about you. As this information modifications, your FICO score tends to alter also. If you don't believe that your FICO scores are essential, reconsider.

The distinction between a FICO score of 620 and 760 can frequently be tens of countless dollars over the life of your loan. A low rating can cost you cash every month or even trigger the house you wish to be unaffordable. Essentially, the higher your FICO scores the less you can anticipate to spend for your loan.

31% $833 700 - 759 2. 54% $858 680 - 699 2. 71% $878 660 - 679 2. 93% $902 640 - 659 3. 36% $953 620 - 639 3. 9% $1,019 As you can see in this example using today's national rates, a person with a FICO rating of 760 or much better will pay $186 less monthly for a $216,000 30-year, fixed-rate home loan than a person with a FICO rating of 620 You can see how essential it is to get your FICO scores in the higher ranges if they are low, and also how crucial it is to keep them high if they are excellent.

Attending to mistakes before you start the process may be frustrating, but handling them while you're in the middle of attempting to buy a home will be downright infuriating. The majority of loan providers use FICO ratings from all 3 credit bureaus when examining your loan application. Your score will likely be various for each credit bureau and there may be mistakes on one that don't appear on the others.

FICO, the California company that arranged the namesake consumer credit rating, uses five key pieces of credit data to identify your credit rating. Your payment history accounts for 35% of your rating, amounts owed accounts for 30% of your rating, length of credit rating accounts for 15%, brand-new credit accounts for 10% of your FICO Score, and lastly, your credit mix accounts for the remaining 10%.

This includes your payment record and your history of on-time and late payments. The second-most essential aspect that impacts your credit report is the amount of money you owe to creditors that makes up 30% of your total score. This looks at your credit utilization rate, which is the amount of offered credit you are utilizing.

About 15% of your credit score is influenced by your credit rating. This includes how long you've had your earliest and latest accounts, and the average age of all your accounts. Likewise considered at 10% is your mix of charge account types. For example, you can have credit cards, retail accounts, mortgage and installment loans.

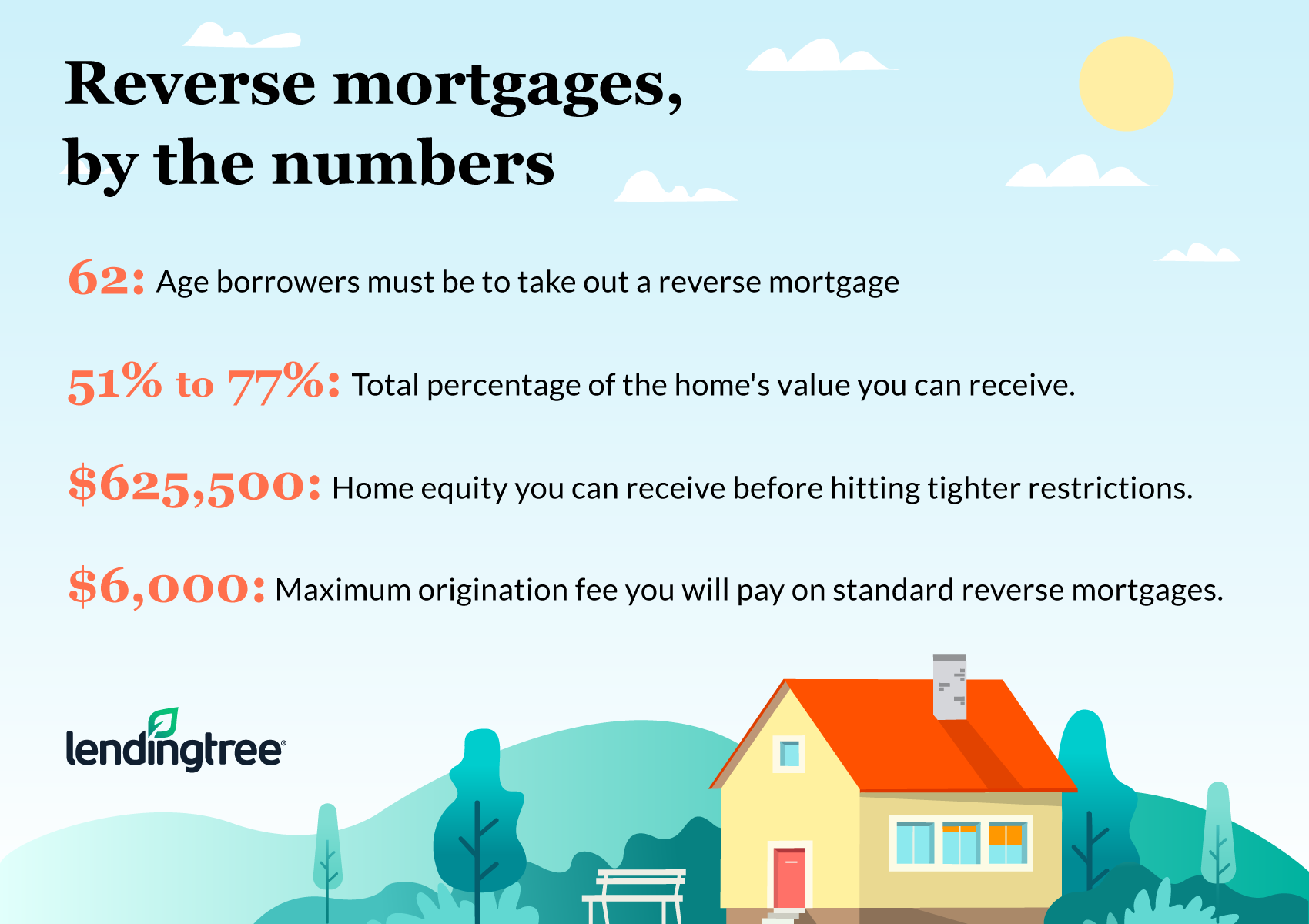

The 9-Minute Rule for Which Of The Following Is Not True About Reverse Annuity Mortgages?

The last 10% of your credit report looks at the number of brand-new credit accounts you've opened just recently. If you submit too numerous inquiries about new charge card, your credit history will be harmed. If you plan to get a home mortgage loan anytime soon, attempt to refrain from opening new charge account, as it will impact your FICO Score. how are adjustable rate mortgages calculated.

e. installation loans and auto loan), and hasn't recently opened brand-new lines of credits or loans would be stated to have a good or exception credit history. Somebody who pays defaults on costs by paying them late, has a high "amounts owed" balance, short credit rating, limited credit types, and has actually just recently inquired about a new credit line would definitely have a poor or bad FICO credit history.

The better your credit score, the more financial chances are offered to you. An excellent or outstanding credit rating can get you access to some of the best credit cards out there, along with lower interest rates on loans and home mortgages. So it makes sense for you to wish to try to get your credit rating as high as possible.

However, some people question if there are likewise ways for you to enhance your credit report by self-reportingthat is, by telling the three credit bureaus about your great financial practices instead of waiting for the details to appear on your credit reports. Your credit report is mainly a record of your payment history on your various credit accounts.

Credit reports likewise include reports on things like insolvencies and tax liens, and can even consist of lease or bill payments. Essentially, your credit report encompasses whatever reported to the consumer credit reporting firms, from payments made to requests for new credit. The 3 primary credit reporting agencies are Equifax, Experian and TransUnion.

Without a credit history, there's no credit history. what is the interest rates on mortgages. Nevertheless, your lenders aren't needed to report your payment history to every credit reporting company. That's why a credit report can vary depending on which credit reporting firm supplies ball game. We have actually got some excellent news and bad news. The bad news is that you can not straight report your financial activity boat timeshare to the three significant credit bureaus.

You need to become a formally acknowledged "information furnisher" in order to report information to the big 3 credit bureaus, and individuals don't get that opportunity. (If you run a small company that allows consumers to bring lines of credit or pay in installments, you could become an information furnisher and pass your consumers' payment histories to the three credit bureaus.) The bright side is that there are still lots of ways to share your positive financial practices with credit bureaus.

The Buzz on What Are Interest Rates Today On Mortgages

Registering for Experian Boost lets you include phone and energy expenses to your Experian report, and a history of on-time payments can boost your credit history. You can also sign up for UltraFICO, a new service that includes your bank account balances in your credit score. That way, a lending institution will know that even if you don't have much of a credit rating, you do have a history of maintaining favorable bank balances (no overdrafts!) and keeping plenty of money on hand.

Know that UltraFICO hasn't completely launched yet, so all you can do right now is register for news and updatesbut it's coming soon!You can even broaden beyond the FICO score and look into alternative reporting methods. The Payment Reporting Builds Credit (PRBC) business bills itself as an "alternative credit movement" and hilton timeshare review creates its own credit rating based upon the bills you currently pay, from phone bills to subscription services.

The very first advantage, naturally, is that your credit history might go up. The other huge advantage of these services is that they can help individuals with minimal or no credit gain access to their first credit card or loanor prove to a landlord that they'll be a good renter. (If you have actually been financially accountable your entire life but have not ever secured a credit card, it's frequently a surprise to discover that loan providers and proprietors may rent my timeshare view you as a credit threat.) There are likewise disadvantages to these services.